How the Iran Conflict Affected Country Risk in Israel and the UAE

How did the armed conflict with Iran affect the country risks of Israel and the Emirates?

One of the indicators of a country's investment attractiveness is the value of the country risk premium (CRP), which is usually calculated based on the yields of government securities on international stock exchanges relative to the long-term obligations of the US Treasury. Since 2004, we have been monitoring the dynamics of country risk values on a monthly basis. For four dozen of the most investment-interesting countries, the calculation results are published in a summary article

.

Strong negative changes in political and economic life, such as military actions, affect the magnitude of country risks. For example, the war in Ukraine has dramatically (by several tens of percent!) increased the country risks of Russia, Ukraine and Belarus. And what was the impact of the beginning of a new (2026) armed conflict in the Middle East?

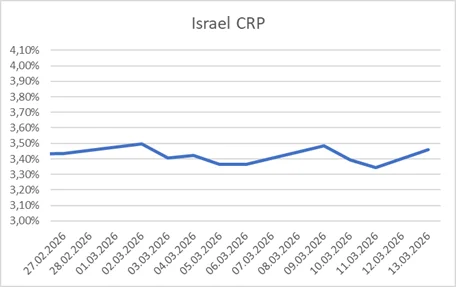

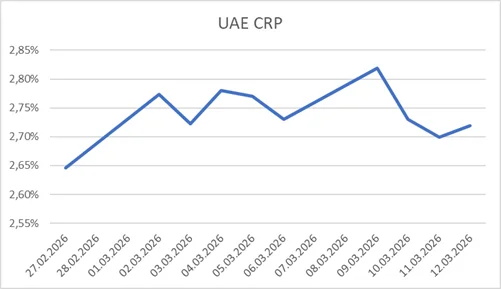

To answer this question, daily research was undertaken on the exchange quotations of government bonds of Israel (due in May 2060) and the United Arab Emirates (due in October 2061), which are well-quoted on all stock exchanges. Data on the dynamics of country risk for Israel and the UAE from February 27 to March 31, 2026 are shown in the graphs below.

Synchronous fluctuations are visible on the charts, and local maximum values are reached almost simultaneously. It is possible to assume a single reason that influenced their appearance.

In general, there is a noticeable trend of a slight increase in the average values of fluctuations, for Israel from about 3.4% to 3.5%, for the UAE from 2.75% to 2.9%. But in general, the changes in the values of the country risk of Israel and the UAE should be considered insignificant. The dynamics of country risks in April confirms this conclusion. As of April 30, for Israel, CRP=3.46%, for the Emirates, CRP=2.81%.

So far, investors do not consider the current political and economic impacts to be significant in long-term planning. Israel and the UAE remain characterized by a low value of country risk, which characterizes the low probability that the investment object will lose value (in full or in part) as a result of the general economic, financial and socio-political factors present in this country regardless of this object.

Author

Prof. Nikolai Trifonov is the Fellow of Royal Institution of Chartered Surveyors, the Full Member of the International Academy of Engineering, the Foreign Member of the Russian Academy of Engineering, the Honorary Appraiser of the Republic of Kazakhstan, teaches real estate appraisal at the Belarusian State Economic University, the author of manuals "The Valuation Theory" and "Comprehensive Real Estate Valuation". In 1994, he founded the Belarusian Real Estate Guild, which united the largest private and state participants in the real estate market and privatization. In 1996, Nikolai created and headed the public association "Belarusian Society of Valuers", which is a member of International Valuation Standards Council (IVSC). In the period 1998-2005 Nikolai was elected and reelected as Board Member of European Real Estate Society (ERES), Director at Large – Responsible for Central & Eastern Europe.